M&A transactions are preceded by lengthy negotiations between the buyer and the seller, where both parties strive for a harmonious outcome. In this multifaceted process, the “earn-out clause” often becomes the focus of negotiations. This seemingly mysterious term is far from merely a simple contractual provision; rather, it acts as a bridge connecting the seller and the buyer, has a profound impact on the course of transactions and shapes the future of businesses transferred into new hands. It also carries the potential to affect both the seller and the buyer. But what exactly is it, why do negotiating parties choose it, and how does it work? Let us take a closer look. The purpose of this article is to make the complex issues surrounding the earn-out clause transparent and understandable. However, it is important to emphasise that earn-out is not a legal concept. The uniqueness of individual business transactions and the different legal environments mean that there is no one-size-fits-all approach. Therefore, every element of an earn-out clause depends on the agreement of the parties, and the structures described below are only generally applicable.

What is an earn-out clause?

Imagine selling your business, the fruit of many years of hard work. You find a buyer, and you both agree on the price. However, there is a twist: part of the payment is tied to how well the business performs after the sale. This additional payment, dependent on future success, is the essence of an earn-out clause. It is a business structure that allows the seller to receive an additional payment beyond the original purchase price, depending on the future performance of the business after the acquisition. It is like a “bonus” for the seller, but tied to the business reaching certain targets after the acquisition, since a certain part, or even the majority, of the purchase price is paid to the seller later in time, only if the actually defined targets are met. From the buyer’s perspective, an earn-out provides greater security when determining the full purchase price, because under an earn-out structure the buyer prices not only the company’s past, but also its post-signing performance. Through the earn-out, the buyer can motivate the seller to continue increasing the company’s profitability after signing the sale and purchase agreement and to help the buyer integrate into the operational management of the acquired company.

Why is it used in acquisitions?

An earn-out provides the buyer with an excellent opportunity for flexible pricing, especially in cases where there is a noticeable difference between the parties regarding the perceived value of the business. In such cases, the earn-out may serve as a compromise that acknowledges the complex challenges involved in forecasting the future of the business, thereby becoming a mechanism that allows the parties to adjust the purchase price after the acquisition based on the actual performance of the business.

The most important and compelling reason why both the seller and the buyer may confidently turn to this contractual structure is their common interest. Both the seller and the buyer have an interest in the success of the business after the acquisition. The earn-out aligns these interests and turns the parties into partners in the continued operation of the business. By applying this contractual structure, the seller becomes interested in actively participating in the company’s handover processes, which can ensure market access for the buyer and the transfer of operational business processes. The seller’s expertise and experience may contribute to the stable operation of the company after the transaction.

In practice, it often happens that in the case of acquisitions of companies with significant business potential or innovative companies, the buyer does not fully buy out the seller, but maintains a minority shareholding in the company for the seller, who remains present as a key person. In general, a key person is someone who has special and indispensable knowledge and experience in relation to the company being sold, and whose replacement would be expensive and time-consuming. This is typically the CEO, the CFO or the CTO. In this way, the buyer can stabilise the acquisition by also motivating the seller who qualifies as a key person to represent and manage the transitional situation necessarily arising from the change of ownership towards both external stakeholders, such as suppliers and customers, and internal stakeholders, such as employees. This enables the buyer to actually take over a business after the acquisition that corresponds to what it could expect for the future based on the company’s past and present, such as previous years’ revenue, EBITDA figures and market presence. This factor is particularly significant from the buyer’s side because, due to the nature of M&A transactions, the buyer’s aim is for the purchase price paid to be recovered in the future from the company’s results. However, the purchase price can only be determined by examining the company’s past, while estimated values regarding the company’s future only serve as guidance. This means that the buyer necessarily assumes significant risks affecting its assets. At the same time, an earn-out may provide assurance that the company will actually perform in the future as expected based on historical data and preliminary estimates.

There is no consensus as to whether the use of an earn-out clause is advantageous or disadvantageous. It has both supporters and opponents, and both sides raise arguments worth considering. The debate surrounding earn-out clauses is therefore quite nuanced and complex. On the one hand, supporters strongly argue in favour of aligning interests and pricing flexibility, emphasising the promotion of a cooperative spirit that can make the seller an active participant in post-acquisition success.

On the other hand, opponents raise legitimate concerns, pointing to the complexity of the structure, since an earn-out may complicate the acquisition agreement. It is not enough to agree only on the purchase price; it is also necessary to agree on certain performance targets, hereinafter referred to as KPIs, and their measurement, because the seller will only be entitled to the amount set out in the earn-out provision if the business has fulfilled the predefined KPIs. The abbreviation KPI comes from the English words Key Performance Indicator, meaning key metrics used to measure the performance of a company or project. These indicators help stakeholders track how the company or project performs compared to previously defined goals. Differences may arise between expectations, which may lead to potential conflicts if the agreement setting out the earn-out has not been properly drafted.

According to Morgan & Westfield, another argument against using an earn-out structure is that predefined KPI metrics can easily be manipulated, which they primarily explain by unclear accounting principles. On the buyer’s side, individual indicators may be manipulated in several ways. If the earn-out amount is linked to the company’s EBITDA, the buyer may reduce the earn-out amount, among other things, by spending excessively on research and development, advertising, marketing or product development, or by paying excessive salaries to “internal” persons. The benefits of these expenses may only appear after several years, but in the present they result in a decrease in EBITDA, thereby benefiting the buyer in the long term. KPI indicators can also be easily manipulated from the seller’s side. If the seller manages the business, it may disregard the company’s long-term strategy and focus on short-term goals by preparing unrealistic forecasts regarding the company’s income, predicting a sudden increase in the company’s income that is significantly higher than reality. In addition, among other things, the seller may relax credit terms provided to itself and customers, thereby resulting in KPI indicators that are less favourable to the buyer.

How does it work?

The use of an earn-out clause requires careful structuring, precise communication and a firm commitment to transparency. As a first step, the parties agree on a base purchase price and determine the potential amount of the earn-out. An essential element of the earn-out structure is the proper definition of the KPIs, as the seller will be entitled to the agreed amount if these are fulfilled. KPIs may include financial targets, market share targets or any other quantifiable indicators of success. The precise definition of these metrics is vital in order to avoid misunderstandings. In practice, the most common approach is to link the KPI to the EBITDA or revenue achieved by the business, although the parties are free to agree on other indicators as well.

The abbreviation “EBITDA” comes from the English expression “Earnings Before Interest, Taxes, Depreciation, and Amortization”. EBITDA is a financial indicator that shows the business performance of a company before tax and financial items, as well as depreciation and amortisation costs, are deducted from the balance sheet. This indicator helps buyers, analysts and managers better understand a company’s operations and profitability without tax and financial policies influencing the results. According to the 2018–Q1 2019 Private Target M&A Deal Points Study prepared by the American Bar Association, approximately 31% of the earn-out provisions examined used EBITDA as the main performance metric, while 29% used the company’s revenue. Given that individual KPIs depend on the agreement of the parties, it is also possible to define several conditions that jointly form the basis for payment of the earn-out amount. In this case, all conditions must be fulfilled during the defined timeframe.

In addition to the earn-out amount and the KPIs, it is also necessary to specify a period during which the KPIs must be fulfilled in order for further payments to be made. Depending on the nature of the business, this period may last for months or even years. According to Morgan & Westfield’s guide to earn-outs, approximately two-thirds of transactions include periods between one and three years. This is important because if the KPIs are fulfilled within the previously defined timeframe, the payment is made to the seller, and the function of the earn-out ceases.

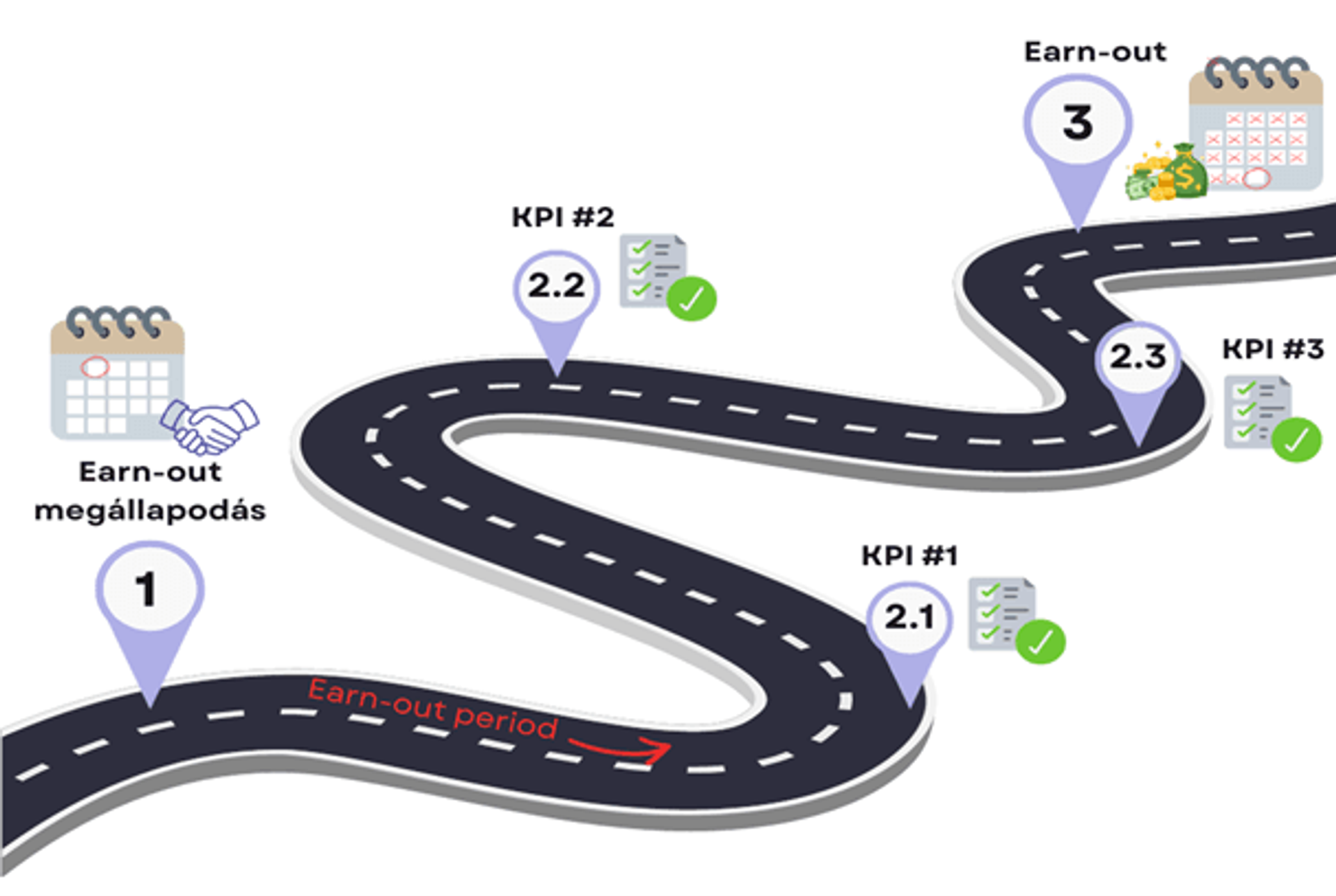

To make the earn-out structure easier to understand, we illustrate the process of an earn-out structure through the following example and diagram.

- acquisition and earn-out agreement, during which, among other things, it is possible to pay part of the purchase price, determine the duration of the earn-out period, define the KPIs and determine the earn-out amount.

- fulfilment of the defined KPIs, which may occur at different times. The parties must define a specific deadline by which the conditions determined as KPIs must be fulfilled.

- payment of the earn-out amount once the KPIs have been fulfilled.

In summary, an earn-out clause is a contractual provision that sets out a mechanism aimed at reducing the uncertainties surrounding the future of a business entering a new ownership structure. It is a compromise tool that allows the seller and the buyer to find common ground during negotiations where there is a difference between perceived values. Moreover, it makes the seller an active participant in the post-acquisition phase, promoting cooperation and shared efforts. An earn-out is advantageous from the buyer’s side because it reduces the risk associated with the business transaction, incentivises the company’s performance and provides flexibility in financing. In addition, it supports the seller’s active participation in the handover process of the company and increases the smoothness of the transition, thereby promoting a successful business transaction and long-term business stability.